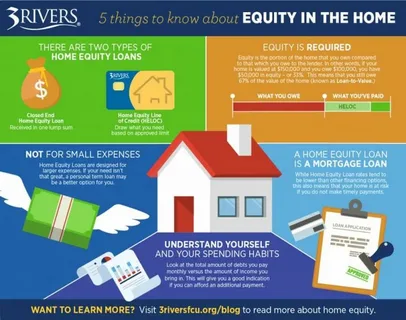

Introduction to Home Equity Loans

A home equity loan is a type of loan that allows homeowners to borrow money using the equity in their homes as collateral. Equity is the difference between your home’s current market value and the remaining balance on your mortgage. Often referred to as a “second mortgage,” home equity loans are an excellent option for funding major expenses, such as home renovations, medical bills, or consolidating debt.

In this guide, we will explore how home equity loans work, their benefits and drawbacks, eligibility requirements, and how to apply.

What Is a Home Equity Loan?

A home equity loan is a lump sum of money borrowed against the equity in your home. It typically has:

- Fixed interest rates: Your monthly payments remain the same.

- Repayment terms: Commonly range from 5 to 30 years.

- Collateral requirement: Your home serves as security for the loan, reducing lender risk but increasing your risk of foreclosure if you default.

How Does a Home Equity Loan Work?

To understand how home equity loans function, consider the following example:

- Your home’s market value: $400,000

- Outstanding mortgage balance: $250,000

- Available equity: $150,000

Most lenders allow you to borrow up to 80–85% of your equity. In this case, you could qualify for a loan ranging between $120,000 and $127,500.

Benefits of Home Equity Loans

Home equity loans offer several advantages, making them a popular financing choice:

- Lower Interest Rates

Compared to personal loans and credit cards, home equity loans usually have lower interest rates due to their secured nature. - Fixed Monthly Payments

Fixed rates mean predictable monthly payments, which simplify budgeting. - Tax Deductibility

Interest payments may be tax-deductible if the loan is used for home improvements (consult a tax advisor for specifics). - Large Borrowing Capacity

You can borrow a significant amount, depending on your home’s equity.

Potential Drawbacks of Home Equity Loans

While beneficial, there are risks associated with home equity loans:

- Risk of Foreclosure

Defaulting on payments can lead to losing your home. - Closing Costs and Fees

Home equity loans often come with closing costs, origination fees, and other expenses. - Over-Borrowing

Borrowing more than necessary can lead to financial strain, especially if the housing market declines and your equity decreases. - Long-Term Debt

Since repayment terms can extend up to 30 years, you may remain in debt for an extended period.

Eligibility Criteria for a Home Equity Loan

To qualify for a home equity loan, you typically need to meet these requirements:

- Sufficient Equity

Most lenders require at least 15–20% equity in your home. - Good Credit Score

A credit score of 620 or higher is often needed, but better scores can secure lower interest rates. - Stable Income

Lenders evaluate your income to ensure you can make monthly payments. - Low Debt-to-Income (DTI) Ratio

A DTI ratio below 43% is generally preferred.

How to Apply for a Home Equity Loan

Here’s a step-by-step guide to applying for a home equity loan:

- Evaluate Your Equity

Calculate your home’s equity by subtracting your mortgage balance from your home’s market value. - Research Lenders

Compare interest rates, fees, and repayment terms from multiple lenders. - Prepare Documentation

Gather necessary documents, such as proof of income, tax returns, and property valuation reports. - Submit an Application

Apply with your chosen lender and await approval. - Close the Loan

Once approved, sign the loan agreement and pay any closing costs to receive the funds.

Alternatives to Home Equity Loans

If a home equity loan doesn’t suit your needs, consider these alternatives:

- Home Equity Line of Credit (HELOC)

A HELOC functions like a credit card, allowing you to draw funds as needed up to a limit. - Cash-Out Refinance

Refinance your existing mortgage for a larger amount and receive the difference in cash. - Personal Loan

An unsecured personal loan may be ideal for smaller borrowing needs. - Reverse Mortgage

For homeowners aged 62 or older, a reverse mortgage allows you to convert home equity into cash without monthly payments.

Tips for Choosing the Right Home Equity Loan

- Shop Around

Compare multiple lenders to find competitive rates and terms. - Read the Fine Print

Understand all fees, penalties, and terms before signing the agreement. - Borrow Responsibly

Only borrow what you need and can comfortably repay. - Consult a Financial Advisor

Seek professional advice to ensure a home equity loan aligns with your financial goals.

Conclusion

A home equity loan can be a powerful financial tool, offering access to funds at lower interest rates than many other options. However, it’s crucial to weigh the benefits and risks carefully and make an informed decision. With proper planning, a home equity loan can help you achieve significant financial milestones while keeping your finances manageable.

If you’re considering a home equity loan, take the time to research lenders, assess your financial situation, and explore alternatives to ensure you choose the best option for your needs.